Hi,

I'm just testing a strategy where I rank the symbols by (for example) ROC, and I ask the top 30.

Then in the Position Sizing blocks, I select to invest 10% of equity, so that I can have a max number of open positions = 10.

And indeed I see in the backtest equity line chart that the max open positions is 10.

At this point I expect that even if I change the top 30 ranked by ROC, to 25 or 20 or (at least) 11, I must have the same results. .

Unfortunately the results change dramatically if I change the top # ranked by ROC, and leaving always the max number of open positions = 10.

So my question is: the max number of open positions don't select the top 10 stocks from the top 30 (or 25 .. or 20 .. and so on) but it follows another criterion that I actually I don't understand. Maybe it is random ?

Does someone know something about, please ?

Thanks so much !!

I'm just testing a strategy where I rank the symbols by (for example) ROC, and I ask the top 30.

Then in the Position Sizing blocks, I select to invest 10% of equity, so that I can have a max number of open positions = 10.

And indeed I see in the backtest equity line chart that the max open positions is 10.

At this point I expect that even if I change the top 30 ranked by ROC, to 25 or 20 or (at least) 11, I must have the same results. .

Unfortunately the results change dramatically if I change the top # ranked by ROC, and leaving always the max number of open positions = 10.

So my question is: the max number of open positions don't select the top 10 stocks from the top 30 (or 25 .. or 20 .. and so on) but it follows another criterion that I actually I don't understand. Maybe it is random ?

Does someone know something about, please ?

Thanks so much !!

Rename

Do you use TransactionWeight to Transport your Rankings to the position sizer?

You could use SignalName (in PlaceTrade()) to show ROC values and Ranking results in the position list.

You could use SignalName (in PlaceTrade()) to show ROC values and Ranking results in the position list.

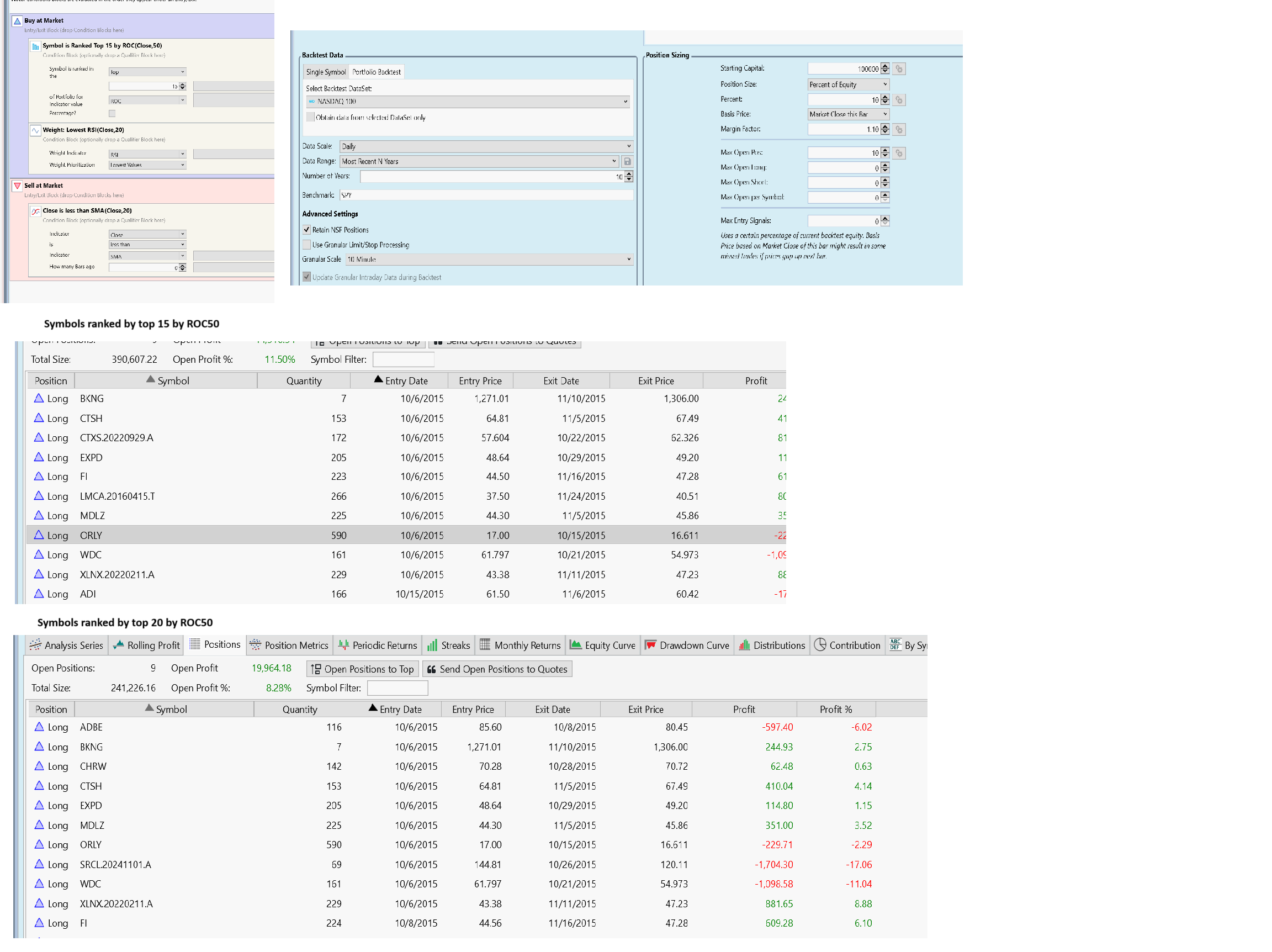

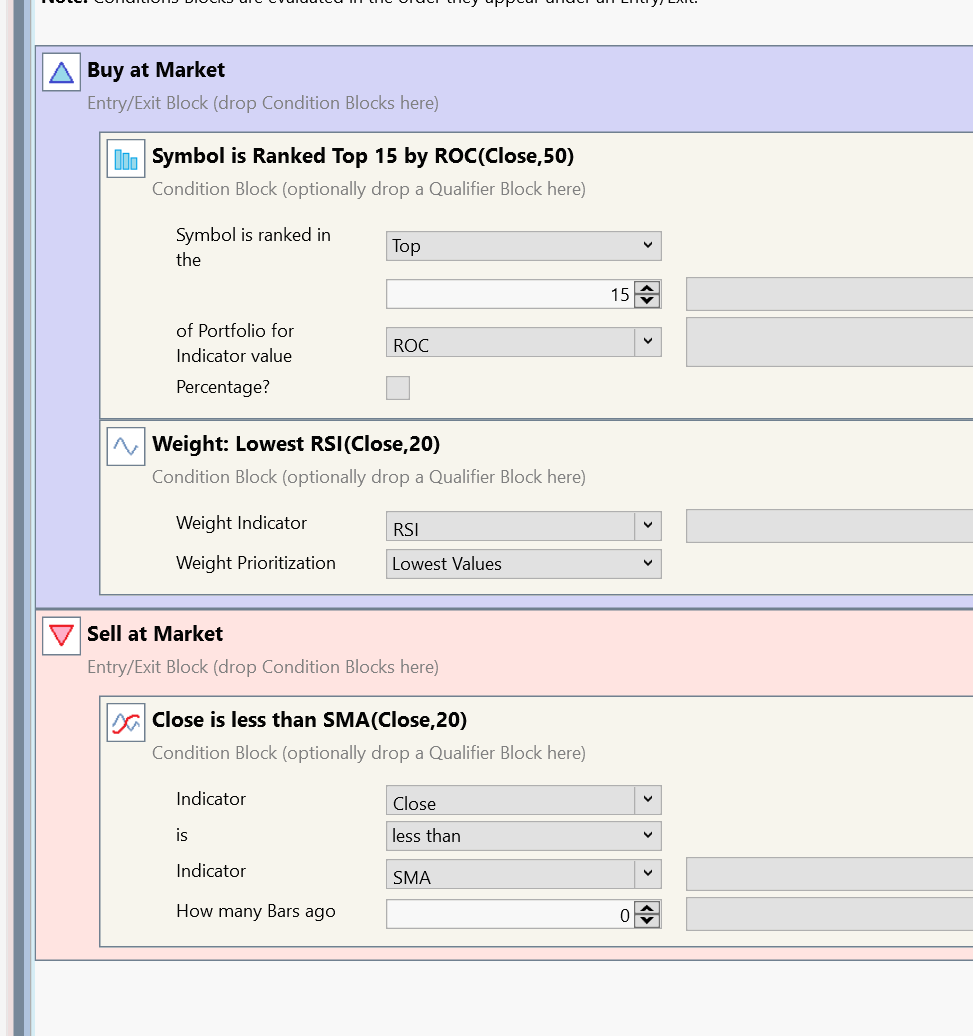

i was able to reproduce this by using the following sample strategy. When I changed the Symbol ranking indicator from top 15 to 20, trades for the FIRST day were quite different (both have 10 positions but came from different tickers)... CAGR increased from 10% to 15%.

Shouldn't this remain the same as long as the max position < the # of top ranking setting?

Shouldn't this remain the same as long as the max position < the # of top ranking setting?

Sorry I was try to make the image smaller so I put them together but the strategy setting is not easy to see. Here it is:

Let me explain a few things:

1. The "Symbol is Ranked..." block selects 15 symbols for the current trading day.

After this step we have a "Portfolio" of 15 symbols.

2. The "Weight" Block assigns weights/priorities to these symbols

After this step we have a sorted list of symbols.

3. The position sizer chooses the 10 symbols with the highest weights.

After this step we have 10 symbols which are actually used to open new positions.

In the scenario discussed here you use ROC for the ranking and RSI for the weight.

This will result in unexpected symbols because a lower ranked symbol may have a better RSI when the number of ranked symbols is increased.

Solution: You should use the same criterion (example: ROC) for ranking and weight to get the results you expect.

1. The "Symbol is Ranked..." block selects 15 symbols for the current trading day.

After this step we have a "Portfolio" of 15 symbols.

2. The "Weight" Block assigns weights/priorities to these symbols

After this step we have a sorted list of symbols.

3. The position sizer chooses the 10 symbols with the highest weights.

After this step we have 10 symbols which are actually used to open new positions.

In the scenario discussed here you use ROC for the ranking and RSI for the weight.

This will result in unexpected symbols because a lower ranked symbol may have a better RSI when the number of ranked symbols is increased.

Solution: You should use the same criterion (example: ROC) for ranking and weight to get the results you expect.

Your Response

Post

Edit Post

Login is required