Buy at market and Sell at market make the Blocks of your intraday trading "strategy". Seriously?

Rename

His strategy is outlined in the description, use ChatGPT to make it more readable. By the way, I had previously published a study on a similar strategy, but this one seems to be an improved version of it

OK but it doesn't make sense to me. Like talking about closing all positions by 3:55 PM to pull out some weekly rebalancing i.e. adjust portfolio allocations every Friday. Huh? Limit to 3-5 trades/day per stock but then you scale into trends with 4 entries? Contradictory again. Once you wade through this wild blend (probably AI assisted) of every trick in the book there's something that looks like a sales pitch in the last sentence.

Eugene, it seems like the first part is the strategy I posted earlier. I’ve attached it again.  9874-ssrn-4824172-pdf

9874-ssrn-4824172-pdf

And the second part appears to be generated by AI.

We definitely need to train some AI on the WL documentation to validate these kinds of concepts.

I tried to implement it using AI before, but not on large caps. I did it based on SSRN, and it didn’t turn out very profitable.

And the second part appears to be generated by AI.

We definitely need to train some AI on the WL documentation to validate these kinds of concepts.

I tried to implement it using AI before, but not on large caps. I did it based on SSRN, and it didn’t turn out very profitable.

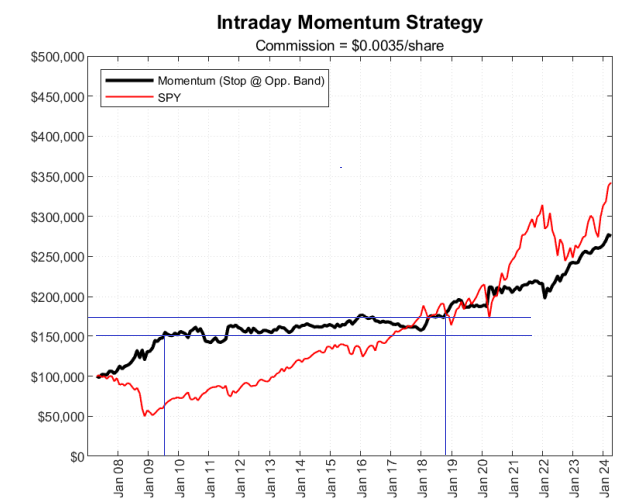

While the concept in the paper might be interesting on an academic level, practically I wouldn't consider it. They cherry picked the starting point against the benchmark at the start of the financial crisis, because if they would have started it 18 months later in March 2009, their result would even look more foolish.

In the 17-year period shown, their strategy turned $100K into about $275, or about 6.1% annualized. Even worse, I marked a 9-year period here where the strategy gained only $25K on $150K. Who would trade that?

In the 17-year period shown, their strategy turned $100K into about $275, or about 6.1% annualized. Even worse, I marked a 9-year period here where the strategy gained only $25K on $150K. Who would trade that?

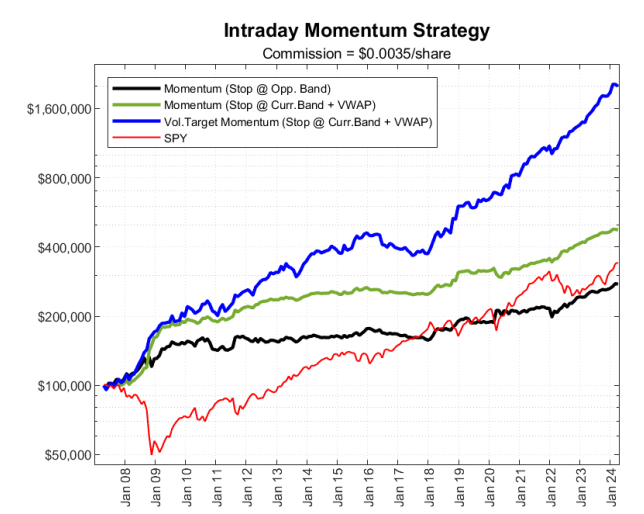

Reading a little further, Fig. 7 shows the result of another version using a stop and VWAP that is actually worth looking into, even though there still a period of nearly 3 years without a new equity high starting in 2016. However, starting in 2018 you get an exponential return, not unlike the 8 years from 2008 to 2016 (blue line) which is apparently due in large part to dynamic position sizing.

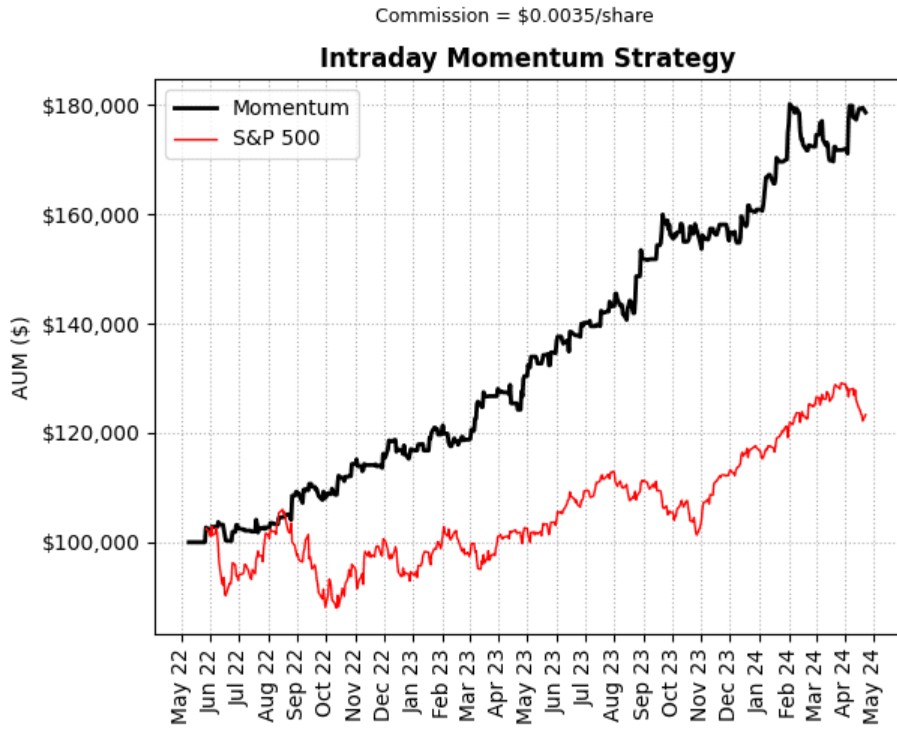

There is code from authors, but I don't trust their tests, I trust my own in WL. Looks like the strategy is still alive, I need to go back, rewrite it, and test it again

https://concretumgroup.com/python-backtesting-beat-the-market-an-effective-intraday-momentum-strategy-for-the-sp500-etf-spy/#Step-1

https://concretumgroup.com/python-backtesting-beat-the-market-an-effective-intraday-momentum-strategy-for-the-sp500-etf-spy/#Step-1

Your Response

Post

Edit Post

Login is required