Hi,

Can someone please tell me if I'm over optimizing this strategy or anything else wrong with it? Ran it for the past 25 years, single etf, but the results are too good to be true.

Can someone please tell me if I'm over optimizing this strategy or anything else wrong with it? Ran it for the past 25 years, single etf, but the results are too good to be true.

Rename

Limit order strategies show unrealistic results when backtested

* on EOD data without granular processing

* with large position size that leads to many NSF positions.

Also: some ETFs have bogus historical data that result in inflated backtest results.

Also: Optimize not on a single 25yr interval. Use several shorter intervals instead and check parameter sets on the remaining intervals. (this is called cross validation).

Conclusion:

* use several ETFs

* use several data providers

* use small position sizes, avoid NSF positions and check profit per trade.

* on EOD data without granular processing

* with large position size that leads to many NSF positions.

Also: some ETFs have bogus historical data that result in inflated backtest results.

Also: Optimize not on a single 25yr interval. Use several shorter intervals instead and check parameter sets on the remaining intervals. (this is called cross validation).

Conclusion:

* use several ETFs

* use several data providers

* use small position sizes, avoid NSF positions and check profit per trade.

Many of the points DrKoch mentioned aren’t applicable because you said you ran it on a single ETF. The best way to know for sure is to try and do some forward testing in either a live or a paper account. Let us know if your real trades match the backtest in the next few weeks!

Thanks!

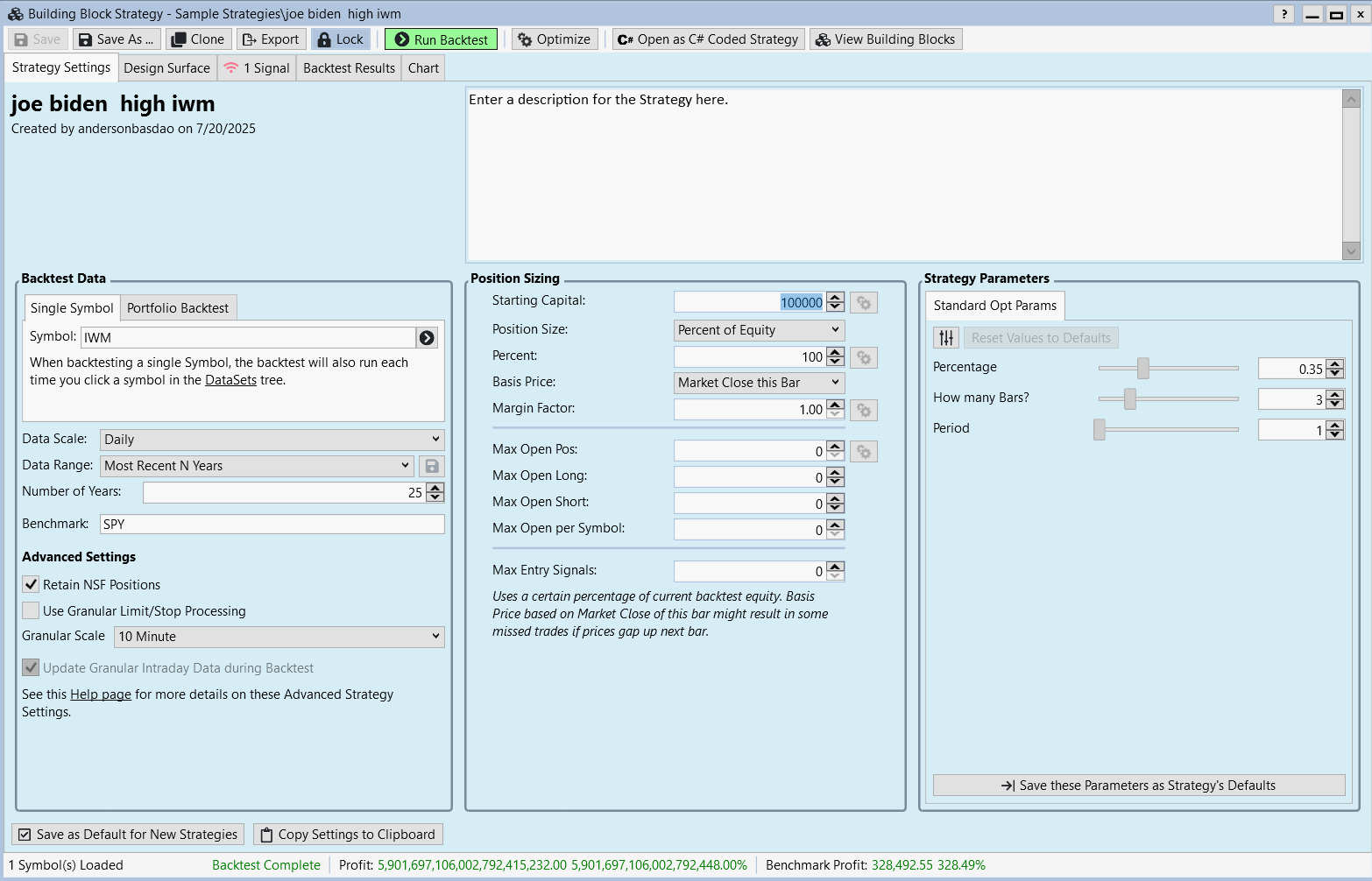

Regarding NSF, I allocate 100% of equity on every trade, for backtest purposes.

I tried many intervals, they all seem to work tremendously well. This is more or less the OPPW strategy, but with targets to enter and exit.

AS far as "granular data", never heard of that. Should I check the option "Use granular limit/stop processing"?

Regarding NSF, I allocate 100% of equity on every trade, for backtest purposes.

I tried many intervals, they all seem to work tremendously well. This is more or less the OPPW strategy, but with targets to enter and exit.

AS far as "granular data", never heard of that. Should I check the option "Use granular limit/stop processing"?

For granular data processing you'll need to use data that support it. For example, 1min, 5min bar data, etc.

If the screenshot shows all the rules and TQQQ is the ticker then I was not able to reproduce this.

If the screenshot shows all the rules and TQQQ is the ticker then I was not able to reproduce this.

Those rules in particular are for IWM.

I got APR of 2.25% for IWM with the above rules for the last 25 years.

Interesting! Here are more snapshots for the last 25 years.

Same as my settings that produced the 2.6% APR.

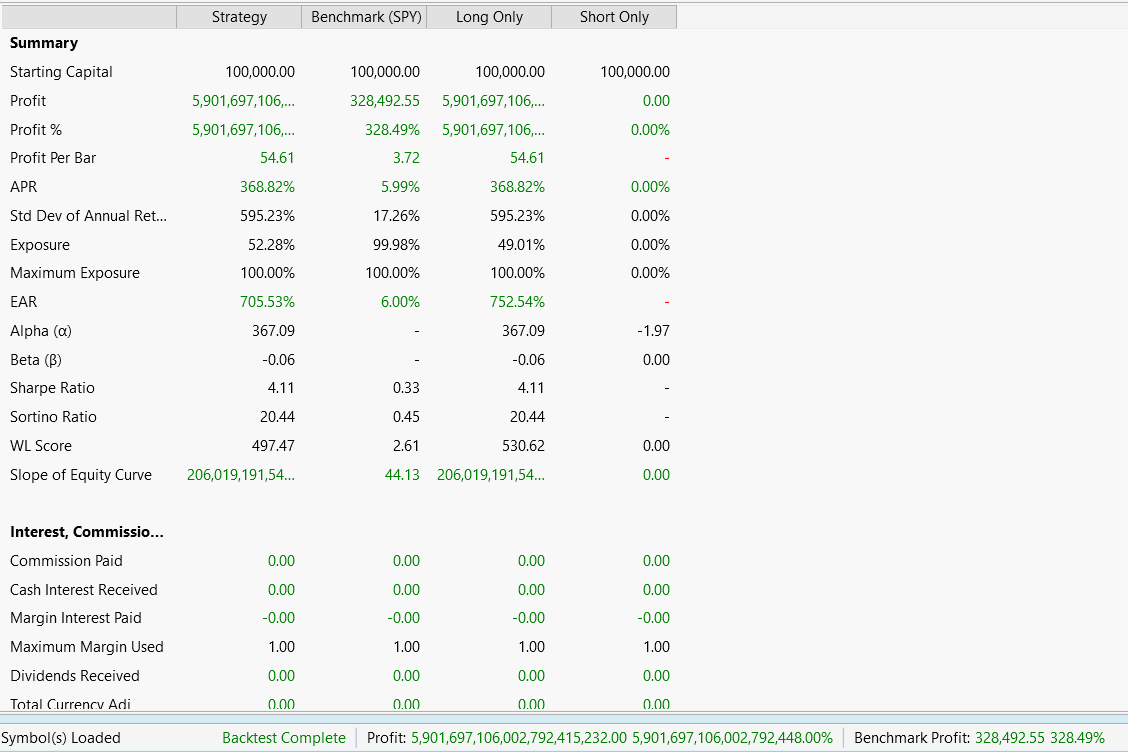

You should be able to look at the list of trades to see what might be wrong. I guess you can not get that 368% APR even you got every daily move up right with your strategy.

You should be able to look at the list of trades to see what might be wrong. I guess you can not get that 368% APR even you got every daily move up right with your strategy.

I did check a lot of them...checked prices on the chart...everything seems right to me.

Are we maybe using different data providers? I don't pay for any third party data, just use whatever comes with WL.

Are we maybe using different data providers? I don't pay for any third party data, just use whatever comes with WL.

Apparently an error in the data. By the way, what data provider is reflected in the strategy chart's status bar where you do a review of all the trades in the most recent 25 years? Try to "Reload chart data from provider" from the right-click context menu.

I did "reload" the data (wealthLab) by right clicking on the chart and now it's a mediocre strategy! I wish I knew this earlier.

Your Response

Post

Edit Post

Login is required