ThetaData is provides professional-grade data for options, stocks, indices, and interest rates data.

- Millisecond latency.

- Unfiltered trade and quote data.

- Historical data for current and expired option contracts.

- Comprehensive Greeks.

The current beta release of WealthLab's ThetaData provider supports scales down to 1-minute intervals an

- ThetaData is a fast and reliable source to drive Quotes, Charts, and the Strategy Monitor

- Use ThetaData as a primary or backup data provider

Click this link to get ThetaData.

Requirements

Install:

- Compatible with WealthLab build 164 (and higher)

- WealthLab's ThetaData Data Extension

- Java 21 or higher: Java 25 (Long-Term Support) recommended.

- ThetaData Terminal - Click Download in the menu at www.thetadata.net and follow the video on Installing Theta Terminal.

Important!

You must complete the Theta Terminal setup successfully once. Your ThetaData credentials will be saved to disk automatically, which will be used by WealthLab's ThetaData extension to launch the Terminal when required.

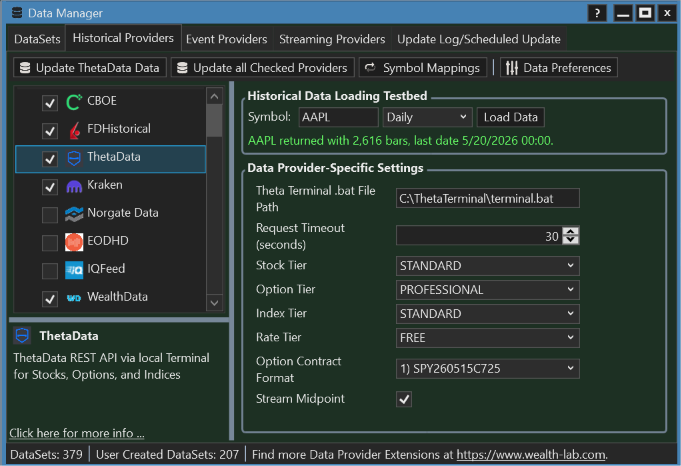

In WealthLab, add a checkmark for ThetaData in Tools > Data Manager > Historical Providers and move it higher in the list according to your data priority preference.

Known Issue(s)

- WealthLab uses ThetaData Terminal v3, for which stock split data is not yet available.

DISCLAIMER:

The third party data is subject to the availability of the respective provider (website) and may be delayed or inaccessible periodically due to network or technical reasons. As the data is not guaranteed to be accurate, it is your responsibility to confirm that it does not contain errors before utilizing it for any type of backtesting or trading activities. Quantacula LLC is not to be held liable for any errors in market data or its inavailability.

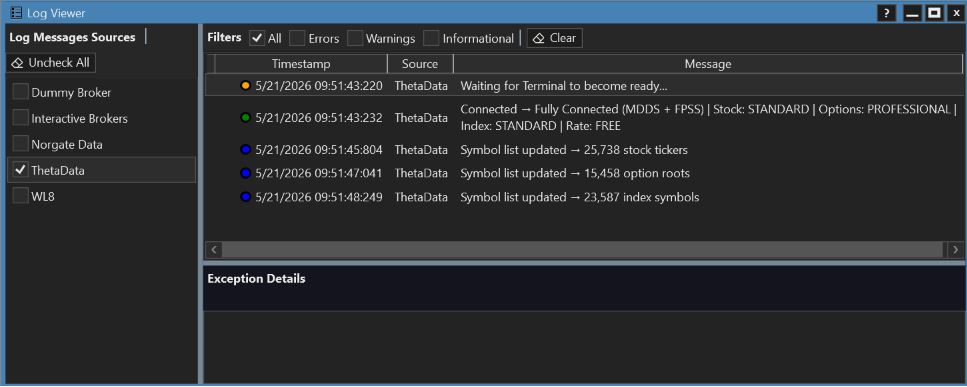

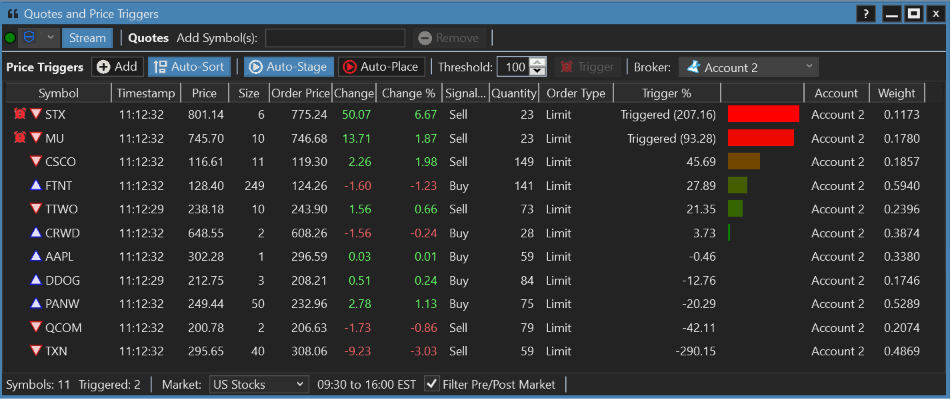

Screenshots

Change Log

- Option data wasn’t requested when the current trading day matched option expiration, fixed.

- Requests for intraday data for the same symbol/scale on the same day were ignored, fixed.

- Requires WL build 168 (min)

- Implemented GetOptionChainSnapshot() as well as a ThetaData overloaded version that returns a

List<ThetaDataOptionGreek>for a specified DateTime (historically) for the underlying's entire option chain by right and expiration. - Optimized requests for GreekHistories for Pro subscriptions.

- A side effect of a change in build 3 caused the current session’s bars and greeks not to be requested during market hours, fixed.

- Requests for “All Data” were unnecessarily re-downloading data.

- Pre/Post (04:00 to 20:00) Intraday data will be retrieved for stocks. A refresh is required to obtain the data for stocks already in the cache.

- Requests for greek histories are no longer made for dates without quotes data.

- Added

GetOptionSymbolAtDelta(), which finds the IV of the ATM contract to use in identifying the contract strike corresponding to the specified delta. - Once synchronized, GreekHistory and an option BarHistory will be returned instantly from the session cache.

- 1-Minute Bid/Ask snapshots are cured for inconsistent data that pops up occasionally (often at 10:00). Our curing algorithm finds the running average spread for the last 5 bars. When a bid/ask spread exceeds 3x the average, the current bid/ask is derived from the previous bar by adding/subtracting the change in underlying x option delta for calls/puts, respectively.

Example:

2025-08-26 09:55 23.34 x 23.42; Underly: 570.46; Δ: 0.448

2025-08-26 09:56 23.38 x 23.45; Underly: 570.49; Δ: 0.448

2025-08-26 09:57 23.30 x 23.38; Underly: 570.31; Δ: 0.447

2025-08-26 09:58 23.30 x 23.37; Underly: 570.32; Δ: 0.447

2025-08-26 09:59 23.27 x 23.33; Underly: 570.25; Δ: 0.447

2025-08-26 10:00 → 21.89 x 24.69; Underly: 570.42; Δ: 0.447 ←

2025-08-26 10:01 23.41 x 23.47; Underly: 570.63; Δ: 0.449

2025-08-26 10:02 23.34 x 23.41; Underly: 570.44; Δ: 0.448

The 21.89 x 24.69 bid/ask at 10:00 would be detected and changed to: 23.35 x 23.41, reflecting the increase in the underlying price x Δ from the previous bar’s bid/ask.

- Likewise, when IV or Theta are found to be 0.0, the values from the previous 1-minute snapshot are inserted for consistency.

- Added

Ratesas an Indicator. - Overhauled Option Chain cache; fixes GetSymbolsOption for weekly Index option expirations.

- Fixed bug requesting strikes over $1,000 (removed the thousands separator).

- Fixed bug that limited data coverage for “PRO” subscriptions.

- Initial release supporting Stocks, Indices, Options. Includes support for historical option chains, option pricing, greeks, and open interest for current and expired contracts!